Updated October 5, 2025 | By Earl | Originally posted February 18, 2019

Imagine this: you’re 40, sipping a cold brew on a beach in Costa Rica, no boss breathing down your neck, no 6 a.m. alarm clock, no soul-crushing 9-to-5. Your bank account? Still growing. Your stress level? Zero. Sounds like a fantasy, right? Wrong! The 4% rule is your golden ticket to making early retirement a reality—without ever worrying about going broke. Forget the “work till 65, pray for Social Security” BS. That’s the trap I fell for when I was clueless about money, blowing cash on dumb stuff like “hot” stocks and overpriced lattes.

Back when I decided to retire early, I was lost. School taught me zip about finances, so I dove into books, blogs, and Reddit threads like a man possessed. After years of trial and error, I found the 4% rule—a dead-simple, research-backed way to withdraw money from your savings without ever running dry. It’s the backbone of financial independence (FI), and it’s how I went from naive to empowered. In this monster guide, I’m spilling everything I’ve learned about the 4% rule, updated for 2025’s wild economy—think $4,000 mortgages, $1,000 grocery bills, and 2.9% inflation. You’ll get a free 4% rule calculator, real-world examples, and tips to dodge the money mistakes I made.

*** Go to my page The Battle-Tested FIRE Calculator Suite: 5 Tools to Plan Your Financial Independence to download your FREE 5 tool calculator and test all these results yourself. These are the same tools I used to achieve Financial Freedom

Ready to have your socks blown off?

Let’s unlock financial freedom and make your retirement dreams real!

What Is the 4% Rule? Your Early Retirement Superpower

The 4% rule is the holy grail of financial independence. It’s a safe withdrawal rate that lets you pull money from your nest egg each year with almost zero chance of going broke—ever. Whether you’re dreaming of quitting your job at 35, traveling the world, or chilling like Lawrence from Office Space (“You don’t need a million dollars to do nothin’, man”), this rule is your roadmap to early retirement.

In plain English: withdraw 4% of your portfolio in year one of retirement, adjust for inflation each year, and your savings should last 30+ years—often forever. It’s backed by over a century of market data and works whether you’re pinching pennies or living large. Let’s dive into why this rule is a game-changer and how you can use it to escape the rat race.

Why “Work Till 65” Is a Total Scam

Google “how long will my savings last?” and you’ll get the same tired advice: slog away until 65, lean on Social Security, and cross your fingers your 401(k) doesn’t tank. That’s not a plan—it’s a gamble. I bought into that nonsense once, thinking retirement was for old folks with bad knees. Spoiler: it’s not. The 4% rule says you can retire whenever your savings hit your FI number, no matter your age. Want to bail at 40? 50? Or just take a year to backpack through Europe? This rule makes it possible.

This isn’t some sketchy get-rich-quick scheme you’d see on Instagram. It’s rooted in hardcore research from financial wizards who’ve crunched numbers through market crashes, wars, and inflation spikes. The 4% rule is your secret weapon to break free from the cubicle, the commute, and the “just one more year” trap. Let’s unpack how it works and why it’s your ticket to financial freedom.

The 4% Rule Explained: How It Keeps Your Money Flowing

The 4% rule is beautifully simple: withdraw 4% of your portfolio in the first year of retirement, adjust that amount for inflation annually, and your money should last 30+ years—often indefinitely. Here’s the breakdown:The Basic Math

- You’ve saved $2,475,000 (we’ll explain this number soon).

- Year 1: Withdraw 4% = $99,000.

- Year 2: Adjust for 3% inflation<15> = $101,970.

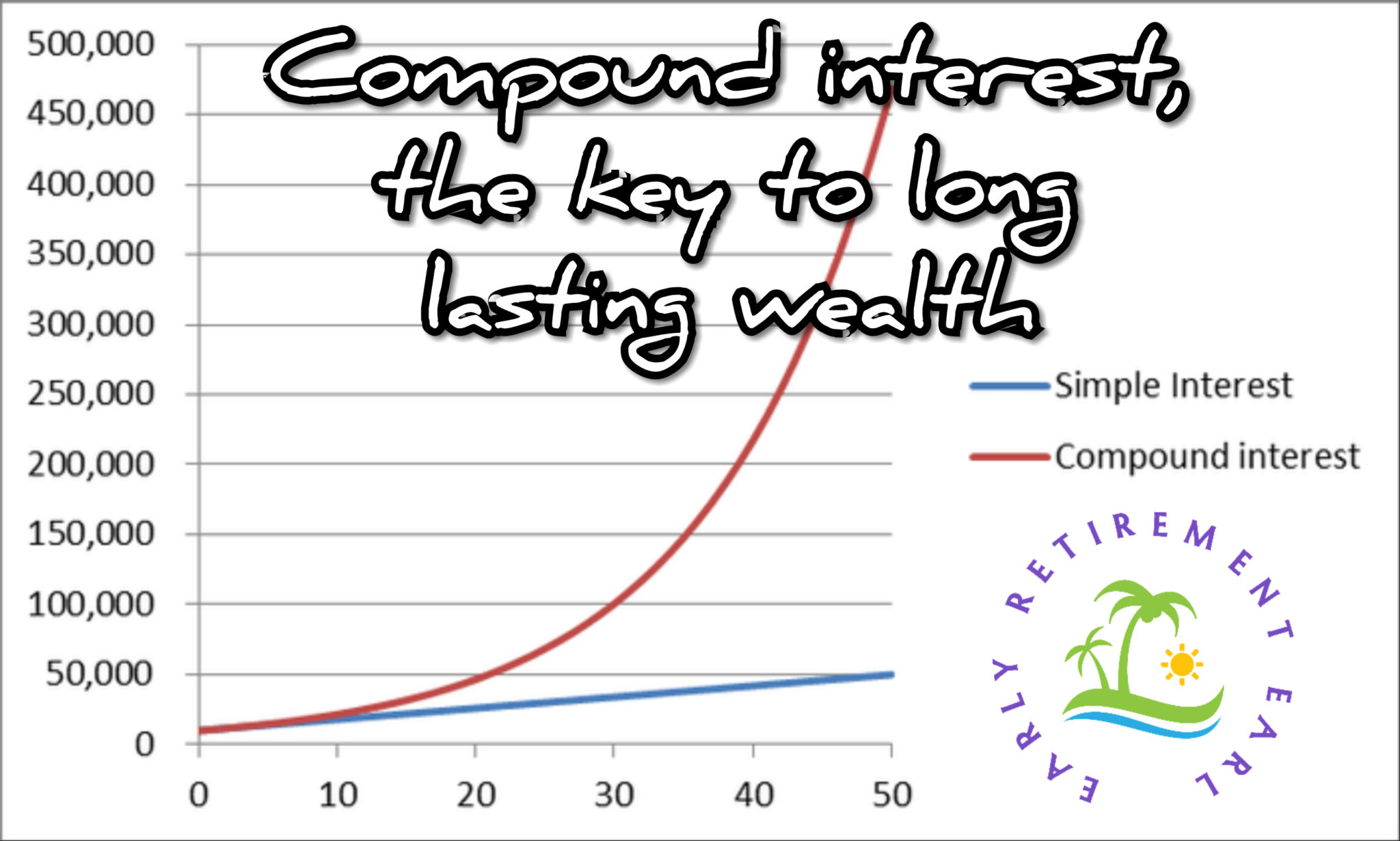

- Invest in a diversified portfolio (think 60% stocks, 40% bonds), earn ~6.5% returns after inflation<10>, and your principal grows, not shrinks.

Why It’s Bulletproof

- Historical Returns: The stock market averages ~7% annual returns after inflation over the long term<10>. With 4% withdrawals, you leave ~3% to cover inflation, keeping your principal intact.

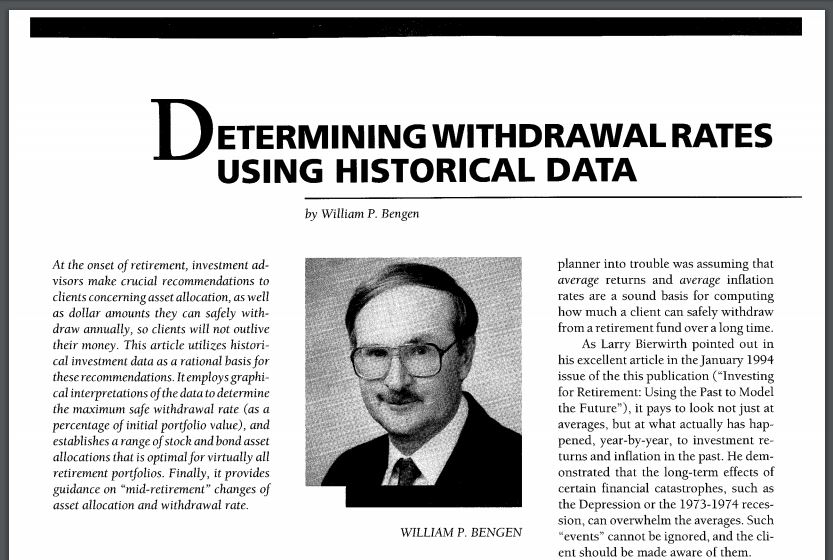

- Research-Backed: In 1994, financial advisor William Bengen analyzed 50 years of market data (1926–1976), including the Great Depression and stagflation. He found 4% withdrawals lasted 33+ years in every scenario. The 1998 Trinity Study (1925–1995) confirmed it: 4% (or 3%) is “extremely unlikely” to deplete a portfolio in 30 years.

- Flexibility: Markets fluctuate, but the 4% rule builds in a safety buffer. Even in bad years, your portfolio survives if you stay disciplined.

2025 Realities: Is 4% Still Safe?

Fast-forward to 2025, and some experts suggest a 3.5% withdrawal rate for extra caution due to:

- Lower Bond Yields: Bonds return less than in the 1990s, reducing portfolio growth<10>.

- Longer Lifespans: Retirees now live into their 90s, needing funds for 40+ years<10>.

- Inflation Spikes: 2025’s 2.9% inflation rate eats more of your returns<15>.

Don’t panic—the 4% rule still holds up, but we’ll show you how to test both 4% and 3.5% ; let’s see the rule in action.

Real-World Example: The 4% Rule in 2025

To make this tangible, let’s use a 2025 budget for a couple planning early retirement, spending $8,250/month or $99,000/year. This reflects today’s higher costs—$2,000 mortgages, $1,000 grocery bills, and more – as outlined in my How to Calculate Your FI Number post.

Step 1: Your FI Number

Using the 25x rule, $99,000/year × 25 = $2,475,000 for a 4% withdrawal rate. For a safer 3.5% rate, it’s $99,000 × 28.6 ≈ $2,831,400. This is your FI number—the savings needed to cover your expenses forever.

Step 2: Your Budget

Here’s the breakdown of that $99,000/year budget, updated for 2025’s realities:

| Expense | Monthly Cost | Annual Cost |

|---|---|---|

| Housing (Mortgage) | $2,000 | $24,000 |

| Property Taxes | $1,000 | $12,000 |

| Healthcare (Pre-Medicare) | $750 | $9,000 |

| Groceries | $1,000 | $12,000 |

| Utilities | $600 | $7,200 |

| Car (Fuel/Maintenance) | $700 | $8,400 |

| Travel/Leisure | $1,200 | $14,400 |

| Hobbies/Entertainment | $300 | $3,600 |

| Insurance | $200 | $2,400 |

| Gifts/Charity | $500 | $6,000 |

| Total | $8,250 | $99,000 |

Step 3: How It Plays Out

Here’s a 30-year projection for a $2.475M portfolio, withdrawing 4% ($99,000) annually, earning 6.5% returns, and adjusting for 3% inflation.

| Year | Starting Balance | Withdrawal (4%) | Earnings (6.5%) | Ending Balance |

|---|---|---|---|---|

| 1 | $2,475,000 | $99,000 | $156,585 | $2,532,585 |

| 2 | $2,532,585 | $101,970 | $160,336 | $2,590,951 |

| 3 | $2,590,951 | $105,029 | $164,039 | $2,649,961 |

| 10 | $2,898,123 | $126,195 | $183,989 | $2,955,917 |

| 20 | $3,183,456 | $181,290 | $201,576 | $3,203,742 |

| 30 | $3,370,000 (approx.) | $240,000 (approx.) | $213,000 (approx.) | $3,343,000 (approx.) |

After 30 years, you’re still sitting on over $3.3M, even with rising costs. That’s the power of the 4% rule—your money grows while you live your dream life!

Try the 3.5% Rule: For extra safety, a $2.83M portfolio withdrawing 3.5% ($99,000/year) yields similar results with even more cushion.

The Science Behind the 4% Rule: Why It’s Virtually Unbreakable

The 4% rule isn’t some random number pulled out of a hat—it’s battle-tested by financial heavyweights. Let’s dive into the research that makes it rock-solid.William Bengen’s 1994 Study

In 1994, financial advisor William Bengen analyzed 50 years of market data (1926–1976), covering brutal periods like the Great Depression and 1970s stagflation. His findings? A 4% withdrawal rate, adjusted for inflation, lasted 33+ years in every scenario, even for a 56-year-old retiree in the worst markets. For luckier years, the money lasted forever. That’s right—your savings could outlive you, no matter how bad things get.

The Trinity Study (1998)

Three finance professors at Trinity University in Texas weren’t convinced by Bengen’s claims, so they ran their own tests using 70 years of data (1925–1995). They mixed portfolios (e.g., 50/50 stocks/bonds, 75/25) and tested withdrawal rates from 3% to 12%. Their conclusion? A 4% rate had a near-100% success rate for 30 years, meaning you’re “extremely unlikely” to run out of money. Even a 3% rate was overkill in most cases.

2025 Updates: Does It Still Hold?

Fast-forward to 2025, and the 4% rule still shines, but experts like Morningstar and Vanguard suggest a 3.5% withdrawal rate for extra safety due to:

- Lower Bond Returns: Bonds yield ~2–3% now vs. 5–6% in the 1990s, slowing portfolio growth.

- Longer Lifespans: Retirees live into their 90s, needing funds for 40+ years.

- Inflation Volatility: Recent inflation hit 2.9% in 2025, up from historical 2–3% averages.

- Market Uncertainty: Post-2020 volatility (e.g., tech crashes, geopolitical risks) raises concerns.

Despite these challenges, recent studies (e.g., Morningstar’s 2024 report) confirm a 4% rate has a 90%+ success rate for 30 years with a 60/40 portfolio. A 3.5% rate pushes that to 95%+. The key? Stay flexible—cut withdrawals in bad years, lean on side income, or use cash buffers.Keywords: 4% rule research, Trinity Study, safe withdrawal rate studies, retirement planning 2025.

5 Common Pitfalls (And How to Dodge Them)

I’ve made enough money mistakes to fill a Reddit thread. (Ever heard of a company called Avant Brands? How about Tattooed Chef? Yeah, I didn’t think so.) Here’s how to avoid screwing up your 4% rule plan:

- Taxes Can Eat Your Withdrawals: Withdrawals from 401(k)s or traditional IRAs are taxed as income. If you need $99,000/year, pull ~$120,000 to cover federal/state taxes (e.g., 20–25% effective rate). Solution: Prioritize Roth IRAs for tax-free withdrawals or brokerage accounts for lower capital gains taxes.

- Healthcare Costs Are Brutal: Pre-Medicare insurance runs $750+/month per person in 2025. Budget at least $9,000/year per person and max out an HSA ($4,300/year for individuals in 2025) for tax-free medical expenses.

- Sequence of Returns Risk: A market crash early in retirement can tank your portfolio. Solution: Keep 1–2 years of expenses ($99,000–$198,000) in cash or bonds to avoid selling stocks during a downturn.

- Lifestyle Creep: Your $99,000 budget can balloon if you start splurging on new cars or exotic trips. Solution: Review your budget annually and cut non-essentials (e.g., $100/month streaming subscriptions add up).

- Inflation Surprises: 2025’s 2.9% inflation means your $99,000 today could be $240,000 in 30 years. Solution: Invest in inflation-protected assets like TIPS or real estate. More tips for dealing with inflation.

Pro Tip: Use geo-arbitrage (moving to a lower-cost area like Boise vs. San Francisco) or a side hustle to lower your FI number or boost income. Flexibility is your superpower. Check out more tips on avoiding lifestyle creep here.

Social Security and the 4% Rule: To Count or Not to Count?

Here’s my take: don’t bank on Social Security. It’s a nice bonus, but with potential benefit cuts by 2035, I leave it out of my 4% calculations. Why? I’d rather plan for the worst and celebrate if it’s there. If you want to include it, here’s how:

- Estimate your payout at SSA.gov (e.g., $2,000/month at 67).

- Subtract it from your annual expenses. Example: $99,000/year – $24,000 (Social Security) = $75,000 needed from savings. New FI number: $75,000 × 25 = $1.875M.

- Alternatively, add Social Security to your 4% withdrawal as extra cushion.

Tread carefully—Social Security’s future is shaky, and early retirees (pre-62) won’t see it for years.

Advanced Strategies to Supercharge the 4% Rule

Want to make the 4% rule even stronger? Here are five pro-level tips to boost your retirement plan:

- Diversify Your Portfolio: A 60/40 stock/bond mix is standard, but add REITs or small-cap stocks for higher returns (7–8% historically<10>). Use low-fee index funds (e.g., Vanguard VTI, expense ratio 0.03%).

- Dynamic Withdrawals: In bad market years, cut withdrawals to 3% or skip inflation adjustments. In boom years, splurge a bit (e.g., 4.5%).

- Side Income: A part-time gig (e.g., freelancing, Airbnb) can reduce your withdrawal rate, extending your portfolio’s life.

- Tax Optimization: Withdraw from taxable accounts first, then Roths, to minimize taxes. Consult a CPA for a personalized plan.

- Ladder Bonds: Create a bond ladder (e.g., 5-year TIPS) to cover 3–5 years of expenses, protecting against early retirement market dips.

These tweaks can push your success rate to 98%+ and let you sleep easy, even in a 2025 economy.Keywords: Retirement portfolio diversification, dynamic withdrawal strategy, tax-efficient retirement.

Tools to Crush Your Retirement Planning

Ready to make the 4% rule work for you? Here’s your toolkit, updated for 2025:

- Free 4% Rule Calculator: The Four Percent Rule Website has a sick calculatior. Be careful, you could lose hours playing with this thing. (https://fourpercentrule.com)

- NerdWallet Budget Worksheet: Align your expenses with the 50/30/20 rule. (https://www.nerdwallet.com/article/finance/budget-worksheet)

- Reddit’s r/financialindependence: Join 1.7M+ members for FI tips and support. (https://www.reddit.com/r/financialindependence/)

- X #FIRE Threads: Search #FinancialIndependence or #4PercentRule for real-time advice and community.

Action Plan:

- Build Your Budget: Estimate Expenses: Eliminate Waste.

- Test the 4% Rule: Determine your FI Number and do the math.

- Invest Smarter: Max out low-fee index funds in a Roth IRA or 401(k).

- Cut One Expense: Skip $10/day dining out ($3,650/year) and invest it.

Why the 4% Rule Will Blow Your Socks Off

The 4% rule isn’t just math—it’s freedom. It’s knowing you can quit your job, travel the world, or build that dream cabin without ever running out of cash. I was once a financial dummy, blowing money on “sure thing” investments and thinking retirement was for grandparents. The 4% rule changed everything, giving me a clear path to financial independence. Now, I’m sharing it with you—especially if you’re as naive as I was.In 2025, with $2,000 mortgages, $1,000 grocery bills, and inflation creeping up<0><20>, the 4% rule is still your best shot at early retirement. It’s backed by 100+ years of data, tested by experts, and flexible enough to handle market crashes, inflation spikes, or unexpected expenses. Whether you want a minimalist van life or a luxurious globetrotting adventure, this rule makes it possible.

Real-Life Stories: How the 4% Rule Changed Lives

To keep you hooked, let’s look at three people who used the 4% rule to transform their lives (inspired by real FIRE stories on Reddit and X):

- Sarah, 38, Former Teacher: Sarah saved $1.5M by 35, living frugally in a mid-cost city. She withdrew 4% ($60,000/year), moved to Portugal (geo-arbitrage), and now teaches yoga part-time. Her portfolio grew to $1.8M by 2025, thanks to market gains.

- Mike, 45, Ex-Engineer: Mike hit $2M and retired in 2023. He uses a 3.5% rate ($70,000/year) to fund travel with his family. A bond ladder protects him from market dips, and he earns $10,000/year from a blog, lowering withdrawals.

- Lisa, 50, Single Mom: Lisa saved $1M and uses 4% ($40,000/year) plus a $20,000/year side hustle to retire early. She downsized to a paid-off condo, cutting her FI number by $500,000.

These stories show the 4% rule’s versatility—frugal or lavish, young or older, it works if you plan smart.Keywords: FIRE success stories, 4% rule real-life examples, early retirement inspiration.

2025 Challenges: Making the 4% Rule Work Today

The 4% rule is timeless, but 2025 brings unique hurdles. Here’s how to tackle them:

Inflation: With inflation at 2.9% in 2025, your $99,000 budget could hit $240,000 in 30 years.

Solution: Invest in stocks (historically outpace inflation) and TIPS. Review your budget annually to avoid overspending.

Healthcare Costs: Pre-Medicare insurance costs $750+/month per person. Early retirees need $18,000/year for a couple.

Solution: Max out HSAs ($4,300/individual, $8,600/family in 2025) and explore ACA subsidies.

Market Volatility: Post-2020 markets are wild—tech crashes, geopolitical risks, and interest rate hikes.

Solution: Diversify with international stocks, keep a cash buffer, and consider a 3.5% rate for extra safety.

Taxes: Withdrawals from 401(k)s are taxed at 20–25% (effective rate).

Solution: Use Roth conversions in low-income years or withdraw from taxable accounts first to minimize taxes.

Busting Myths About the 4% Rule

The 4% rule has critics, but most objections are overblown. Let’s debunk common myths:

- Myth: “It’s too risky in today’s market.”

Truth: Even with 2025’s lower bond yields, a 4% rate has a 90%+ success rate over 30 years<10>. A 3.5% rate pushes it to 95%+. - Myth: “Inflation will destroy it.”

Truth: The 4% rule adjusts for inflation, and diversified portfolios historically beat inflation by 4–5%. - Myth: “It only works for millionaires.”

Truth: Frugal retirees can hit FI with $1M or less (e.g., $40,000/year × 25 = $1M). Geo-arbitrage or side hustles make it even easier. - Myth: “It’s too simple.”

Truth: Simplicity is its strength. The Trinity Study tested countless scenarios, proving 4% is robust yet flexible.

How to Start Using the 4% Rule Today

Ready to make the 4% rule your superpower? Follow these steps:

- Calculate Your FI Number: Use my [FI Budget Template](link to previous post) to estimate expenses ($99,000/year?). Multiply by 25 (or 28.6 for 3.5%).

- Test Your Plan: Plug your numbers into my [4% Rule Calculator] to see how long your savings last.

- Build Your Portfolio: Invest in low-fee index funds (e.g., Vanguard VTI, 0.03% expense ratio) for 7% average returns.

- Cut Expenses: Save $10/day ($3,650/year) by cooking at home or canceling subscriptions, and invest the difference.

- Stay Flexible: Adjust withdrawals in bad years, add side income, or relocate to a lower-cost area.

Pro Tip: Start small. Even $100/month invested at 7% grows to $150,000 in 30 years. Every dollar counts toward your FI number.Keywords: How to use 4% rule, early retirement steps, FI investment strategies.

Community and Resources:

Join the FIRE MovementThe 4% rule is your foundation, but the FIRE (Financial Independence, Retire Early) community can supercharge your journey. Here’s how to dive in:

- Reddit’s r/financialindependence: 1.7M+ members share tips, success stories, and budget hacks. (https://www.reddit.com/r/financialindependence/)

- X #FIRE Threads: Search #FinancialIndependence or #4PercentRule for real-time advice. Follow me (@EarlsFIJourney) for daily tips.

- Mr. Money Mustache Blog: A FIRE classic with practical advice. (https://www.mrmoneymustache.com/)

- ChooseFI Podcast: Free episodes on FI strategies. (https://www.choosefi.com/)

Free Tools:

- [4% Rule Calculator]: My downloadable spreadsheet to test withdrawals.

- Goodbudget App: Free envelope budgeting for expense tracking. (https://goodbudget.com/)

Why the 4% Rule Will Change Your Life

The 4% rule isn’t just a number—it’s freedom. It’s waking up without an alarm, pursuing your passions, or telling your boss “I’m out” without fear. I was once a financial newbie, wasting money on “sure thing” stocks and thinking retirement was decades away. The 4% rule gave me clarity, a plan, and a path to financial independence. Now, I’m sharing it with you—especially if you’re as naive as I was.In 2025, with $4,000 mortgages, $1,000 grocery bills, and inflation creeping up, the 4% rule is still your best shot at early retirement. It’s backed by 100+ years of data, tested by experts, and flexible enough to handle market crashes, healthcare costs, or tax surprises. Whether you’re dreaming of a minimalist van life or a jet-setting adventure, this rule makes it real.

Take Action: Make Your Money Last ForeverDon’t let retirement planning scare you. Start today:

- Build Your Budget: Use my [FI Budget Template](link to previous post) to nail down expenses.

- Test the 4% Rule: Plug your numbers into my [4% Rule Calculator].

- Save Smarter: Cut one expense ($10/day = $3,650/year) and invest it in index funds.

- Join the Conversation: Share your retirement dream—beach house or mountain cabin?—in the comments or on X (@EarlsFIJourney). Got a money question? Ask away!

Free FI Starter Kit: Check back here frequently (earlyretirementearl.com) and follow me on X for exclusive tips to supercharge your FI journey.

Let’s make your savings last forever.

Happy planning,

Earl

_______________________________________________________________________________________________

Original Post from February 2019 Below

When I first made the decision that I was going to retire early I had no idea where to start. So I read. I read a lot. I spent the next several years committed to teaching myself what the school had failed to teach me. How to properly plan our finances so we don’t have to work forever. I continue to learn to this day. But I have long since answered the question of how long my savings will last. The key lies within the 4% rule.

Your savings will last forever as long as you follow the 4% rule. Live within your means. Spend less than you earn. This is true of your working years and even more so in retirement. Luckily, there is another simple mathematical rule that you can follow to assure you succeed at this.

The 4% rule.

What follows is the result of my years of research and personal financial development. This is what I like to call the simplified and definitive guide to the 4% rule.

What is the 4% Rule?

The 4% rule is a guide or general rule of thumb for the safe withdrawal rate of a retiree from their nest egg. The purpose of the 4% rule is to provide the retiree with a steady annual income stream with the lowest probability of depleting funds entirely.

In simpler terms, the 4% rule aims to figure out how much money you can spend from your nest egg each year while assuring you do not run out of money before you die.

Origin of the 4% rule

In 1994, financial adviser William Bangen used historical data from the 50 year period from 1926 to 1976 to conduct a thorough study. The goal of the study was to determine the best withdrawal rates for retirees. Bengen concluded that there was no historical case during the 50 year period he studied, in which the 4% annual withdrawal rate would have exhausted a portfolio in less than 33 years.

What this means is that even in the worst case scenario from the year 1926 – 1976, if you followed the 4% rule, you would last 33 years before running out of money. So the unluckiest 56 year old to retire during those years ran out of money at age 93.

Bengen also found that in the best of years, the money would last forever. So the luckiest 30 year old retiree never had to worry about money again provided they followed the 4% rule

How does the 4% rule work?

The premise of the 4% rule seems simple enough. Withdraw 4% or less of your savings every year and never run out of money. But how does this work? You could trust the validity of past research or you could dig into it yourself to understand the inner workings. Since this is our life savings we are talking about, lets dig deeper.

On its surface, the 4 % rule makes little sense mathematically. If you have $100 and spend 4% or $4 every year, your money would be gone in 25 years. You need to factor in the interest that your money should be earning.

The stock market has historically averaged over 7% annually over the last 100 years.

Assumptions

The 4% rule assumes those historical averages will continue. So if you have One million dollars the year prior to your retirement, and you earn 7%, you will have $1,070,000 at the end of the year. If you withdraw 4% or $42,800, that leaves you with $1,027,200.

You actually end the year with MORE than you started.

You may be saying this doesn’t make sense and you are right. Why the surplus?

Inflation

Historical inflation rates in the US are universally recognized as being between 2% and 3%. For the purposes of playing it safe, we go with an estimate of 3%.

If you are earning 7% in interest annually but 3% is eaten away by inflation, that leaves 4% for withdrawals. As long as the historical averages continue to hold up, and you never withdraw more than 4%, you will never need to touch the principal. You will therefore never run out of money.

When Bengen first published his 4% rule it was, predictably, met with skepticism. I myself had a hard time believing just how simple this all could be. Markets fluctuate and inflation is never steady. I had spent so many years simply being intimidated by the overwhelming idea of figuring out my financial future. I could hardly believe it was this simple all along.

The Trinity Study

In 1998, three finance professors at Trinity University in San Antonio Texas decided to determine the validity of Bengen’s original research. Their primary concern was the irregularity with which stock s grow and/or shrink over time.

One of their main requirements for validation of Bengen’s study was that a portfolio would need to last at least 30 years without becoming fully depleted.

The authors back tested a number of withdrawal rates and investment mixes covering a period of 70 years vs. Bengen’s 50 years. they used historical stock market data from the years 1925 – 1995.

They concluded that Bengen’s results remained valid even 20 years after his original work. In their conclusion they wrote “If history is any guide for the future, then withdrawal rates of 3% and 4% are extremely unlikely to exhaust any portfolio of stocks and bonds. In those cases success seems to be assured.”

Success meaning little to no likelihood that an account following the 4% withdrawal rate would be depleted within 30 years.

The Trinity Study had used current data to validate the 4% rule. In the 20 plus years since, numerous others have duplicated the study to similar results.

Planning and the 4% rule

The authors of the Trinity Study did make one caveat in the form of the following qualification…

“The word planning is emphasized because of the great uncertainties in the sock and bond markets. Mid-course corrections likely will be required, with the actual dollar amounts withdrawn adjusted downward or upward relative to the plan. The investor needs to keep in mind that selection of a withdrawal rate is not a matter of contract but rather a matter of planning”

Basically what they were saying is that they recognize the importance of being flexible in your approach as well as the importance of the willingness to change course when required.

The 4% rule works best as a general guide, not as a concrete rule.

I have found the 4% rule an invaluable part of my plan. You can use it as a guide to in planning your monthly withdrawals from a nest egg or as a guide to determine how the size nest egg you require based on your expected annual spending.

So for example, if I want to be able to spend $100,000 a year in retirement, I can perform some simple math to determine I will need a nest egg of $2,500,000. Conversely, if based on my current savings rates I can expect to have a nest egg of $1,500,000, I know my withdrawals will be about $60,000 annually.

There are also some other factors I have researched that will impact my use of the 4% rule in retirement.

How do taxes impact your use of the 4% rule in retirement?

Your retirement nest egg will most certainly be comprised of various accounts. Some combination of a 401k plan, a Roth IRA, pension plan, savings accounts, etc. Taxes will impact some of these accounts far differently than others.

For example, if you are planning on taking withdrawals from a 401k plan, you need to be prepared to pay the income tax that you have deferred while you were making those tax free contributions. Conversely, if you have a simple savings or brokerage account you have likely already paid your income taxes on that money. You will be looking at much lower rates for capital gains or dividends then a straight income tax.

You will need to be careful when planning your safe withdrawal rate here. If you are expecting to spend $40,000 a year and that is exactly what 4% of your 401k is, you will need to make some adjustments. That $40,000 will become quite a bit less once income tax is removed.

Should I include Social Security in my 4% withdrawal rate?

One factor that neither Bengen nor the Trinity Study examined was social security. There has been no study I know of which can guide you on how to factor Social Security into your safe withdrawal rate.

My personal feelings on Social Security; If it is there for me then I will consider it a bonus after the fact. I am not including it into any of my calculations when planning for retirement.

One way to factor in Social Security; You could use historical rates to estimate what your monthly payout will be. You can then then add it to your 4% withdrawal.

Final thoughts – Does the 4% rule really work?

In this article I have defined what the 4% rule is and explained its origins. You should now have a good understanding of how it is intended to be used. Also, its place is in history with financial experts. But does it really work?

The answer to the question does the 4% rule really work is that it is entirely up to the user. If used correctly, the 4% can clearly give the user a safe rate of withdrawal that will allow them to feel a sense of security throughout retirement that their funds will never be depleted prematurely.

There are numerous variables that each individual will need to take in to account when deploying any retirement plan. The 4% rule is as solid, as any I have ever seen. in fact it is the most solid. Backed by over 100 years of data and numerous studies at the university level.

What is important is that you are thinking about this ahead of time. Furthermore, you must be doing everything you can to plan now so you won’t regret it later. You are in full control of the type of retirement you have. Weather you want to save an enormous nest egg and live it up in retirement with large annual distributions or you are trying to get out of the rat race as young as possible and are willing to sacrifice luxury and live a life of frugality, the 4% rule can help you.

Final Conclusion

Does the 4% rule work? Absolutely, unequivocally, YES!

If you are following it’s intended use and making adjustments as you go, you should be able to use the 4% rule to assure you will never run out of money in retirement.

Stop Guessing at Your Retirement

This post is just one piece of the puzzle. I’ve put my entire $2M blueprint into a free 48-lesson Financial Literacy Course specifically for late-starters. No fluff, just the math you need to catch up and win.

The Financial Freedom Compass: A Financial Literacy CourseEarl

He didn't just save his way to freedom; he built a compounding engine. By combining "Bogleheads" index investing with a conservative options strategy, Earl turned a late start into a total victory. He’s not just talking theory—he’s living the math. Last year alone, Earl generated $78k in options premiums via the "Wheel" strategy and ~$400/month in passive dividends, proving that liquidity is the true key to quitting early.

Launched in 2019, EarlyRetirementEarl.com is a no-BS zone for dads and late-starters who want actionable, battle-tested steps to freedom. Featured on ThinkSaveRetire, ESI Money, Budgets are Sexy, and Camp Fire Finance, Earl’s mission is to share the financial literacy he was never taught in school. No fluff, no gurus—just the math.

Not financial advice. I’m not a CFP or licensed advisor. All numbers are historical; markets fluctuate. Past performance is not indicative of future results. Do your own research and consult a professional.