Nobody ever got rich on accident!

Anyone can quit their job and say they are retired. The key to retiring early is to assure you have enough money to stay retired. In order to successfully accomplish this you must have a strategy.

Introduction: Why FIRE Investment Strategies Are Your Path to Freedom

Nobody achieves financial independence by accident. Early retirement requires a strategic plan of attack filled with timely, achievable goals along the way to your ultimate goal of financial independence; At its core are FIRE investment strategies that grow a sustainable nest egg. The Financial Independence, Retire Early (FIRE) movement empowers you to quit the rat race—whether that’s a 9-5 or side hustle—by building wealth through smart investing. In 2025, with 3-4% inflation (Federal Reserve) and evolving markets, the right investments can make a $1M portfolio by 2030 achievable for disciplined savers.

This guide focuses on investment strategies to reach FIRE: index funds for growth, dividend ETFs for passive income, real estate for diversification, and bonds for stability. We’ll cover calculating your FIRE number, optimizing your portfolio, and leveraging 2025 market trends. D

Ready to build your early retirement investment plan? Let’s dive in!

Step 1: Calculate Your FIRE Number to Guide Investments

Your FIRE investment strategies begin with your FIRE number—the portfolio size needed to live off investments indefinitely. This sets the target for your investment plan.

How to Calculate It

The 4% rule, backed by the Trinity Study Baylor University, suggests you can withdraw 4% of your portfolio annually for decades. Here’s the process:

- Estimate Annual Expenses: Track spending for 3-6 months using YNAB or Mint. Include taxes, health insurance, and lifestyle costs. Example: $40,000/year.

- Multiply by 25: $40,000 × 25 = $1M. This is your FIRE number for full financial independence.

- Adjust for Income: If you expect $10,000/year from side gigs or pensions post-FIRE, subtract $250,000 ($10,000 × 25).

- Factor in 2025 Inflation: With 3-4% inflation projected Federal Reserve, lean FIRE ($750k) or fat FIRE ($1.5M+) may suit your goals.

Example: At 35, Emma spends $50,000/year. Her FIRE number is $1.25M. By investing $25,000/year at 7% returns, she reaches her goal in ~15 years Vanguard Calculator.

Pro Tip: Use Engaging Data’s FIRE Simulator to model scenarios with market fluctuations.

Step 2: Index Funds – The Foundation of FIRE Wealth

Index funds are the cornerstone of most FIRE investment strategies, offering low-cost, diversified growth to build your portfolio efficiently.Why Index Funds?

- Historical Returns: 6-8% annually (S&P 500 average, 1928-2025, adjusted for 2025 projections per Morningstar).

- Low Fees: Expense ratios of 0.03-0.1% (vs. 1% for managed funds) keep more money compounding.

- Diversification: One fund covers thousands of stocks, reducing risk.

Top Index Funds for 2025

- Vanguard VTI: Tracks the total US stock market (0.03% fee). A $10,000 investment at 7% grows to $19,672 in 10 years Bankrate Calculator.

- Fidelity FZROX: Zero-fee total market fund, maximizing returns.

- Schwab SWTSX: Broad exposure (0.03% fee), available via Schwab.

How to Invest for FIRE

- Allocate 60-80%: Put most of your portfolio in index funds for long-term growth.

- Dollar-Cost Averaging: Invest fixed amounts monthly (e.g., $500) via M1 Finance to smooth out market volatility.

- Rebalance Annually: Sell gains to maintain allocation, especially with 2025’s projected 10% market correction JPMorgan.

Example: Investing $20,000/year in VTI at 7% grows to $500,000 in 15 years, nearly half a $1M FIRE goal.

Step 3: Dividend ETFs – Passive Income for FIRE

Dividend-paying investments are a FIRE favorite for generating passive income for FIRE without selling assets.

Why Dividend ETFs?

- Cash Flow: Quarterly dividends fund living expenses, ideal for Barista FIRE (part-time work post-FIRE).

- Stability: Less volatile than growth stocks, protecting your nest egg.

- Tax Efficiency: Qualified dividends are taxed at 15% (vs. 24% ordinary income for many).

Top Dividend ETFs for 2025

- Vanguard VYM: 2.5% yield, pays $25,000/year on a $1M portfolio (0.06% fee).

- Schwab SCHD: 3% yield, $30,000/year on $1M (0.06% fee).

- SPDR SPYD: 4% yield, higher risk but $40,000/year on $1M.

How to Invest for FIRE

- Allocate 10-20%: Balance with index funds for growth.

- Reinvest Dividends: Until FIRE, reinvest to compound returns.

- Tax Strategy: Hold in a Roth IRA to avoid taxes on dividends Fidelity.

Example: A $200,000 investment in SCHD yields $6,000/year, covering 15% of a $40,000/year FIRE budget.

Internal Link: Living Off Dividends in Retirement

Step 4: Blue-Chip Stocks – Stability and Growth

Blue-chip stocks remain a key part of a financial independence investments plan for their reliability and dividends

Why Blue-Chip Stocks?

- Stability: Resilient during downturns (e.g., 2008, 2020).

- Dividends: Pay 2-3% yields, adding passive income.

- Growth: Average 6-8% annual returns, complementing index funds.

Top Blue-Chip Stocks for 2025

- Johnson & Johnson (JNJ): Healthcare, 2.7% yield, steady growth.

- Procter & Gamble (PG): Consumer goods, 2.4% yield, recession-resistant.

- Microsoft (MSFT): Tech, 0.8% yield but high growth (10%+ annually).

How to Invest for FIRE

- Allocate 10-20%: Balance with index funds and ETFs.

- Buy and Hold: Use M1 Finance for fractional shares and auto-investing.

- Diversify: Spread across sectors (healthcare, tech, consumer goods).

Example: $50,000 in JNJ yields $1,350/year and grows to $98,360 in 10 years at 7%.

Link: How to Build a Blue-Chip Stock Portfolio

Step 5: Real Estate – Diversification for FIRE

Real estate adds diversification to your FIRE investment strategies, offering income and growth without the hassle of being a landlord.

Why Real Estate?

- Income: Real Estate Investment Trusts (REITs) pay 3-4% dividends.

- Growth: Historical 8%+ returns (Nareit, 1972-2025).

- Inflation Hedge: Rents rise with 3-4% inflation in 2025.

Top REITs for 2025

- Vanguard VNQ: Diversified REIT ETF, 3.5% yield, 0.12% fee.

- Realty Income (O): Monthly dividends, 5% yield, retail focus.

- Prologis (PLD): Logistics REIT, 2.8% yield, tied to e-commerce growth.

How to Invest for FIRE

- Allocate 5-15%: Limit exposure to balance risk.

- Use Tax-Advantaged Accounts: Hold in a Roth IRA to avoid dividend taxes.

- Start Small: Invest $1,000 via Schwab for fractional shares.

Example: $100,000 in VNQ yields $3,500/year and grows to $196,720 in 10 years at 7%.

Keyword Focus: retirement investing 2025

Step 6: Bonds – Stability for 2025 Volatility

With 2025’s projected 10% market correction, bonds add stability to your early retirement investment plan.

Why Bonds?

- Safety: Lower risk than stocks, preserving capital.

- Income: Fixed yields for predictable cash flow.

- Inflation Protection: Treasury Inflation-Protected Securities (TIPS) adjust with CPI.

Top Bonds for 2025

- TIPS: Yield ~1% + inflation adjustment (3-4% in 2025).

- Vanguard BND: Total bond ETF, 3% yield, 0.03% fee.

- iShares IEF: 7-10 year Treasuries, 2.5% yield, low volatility.

How to Invest for FIRE

- Allocate 5-10%: Increase to 20% as you near FIRE.

- Ladder Maturities: Spread across 1-10 year bonds to manage interest rate risk.

- Buy via ETFs: Use Vanguard for low fees.

Example: $50,000 in BND yields $1,500/year, stabilizing your portfolio during market dips.

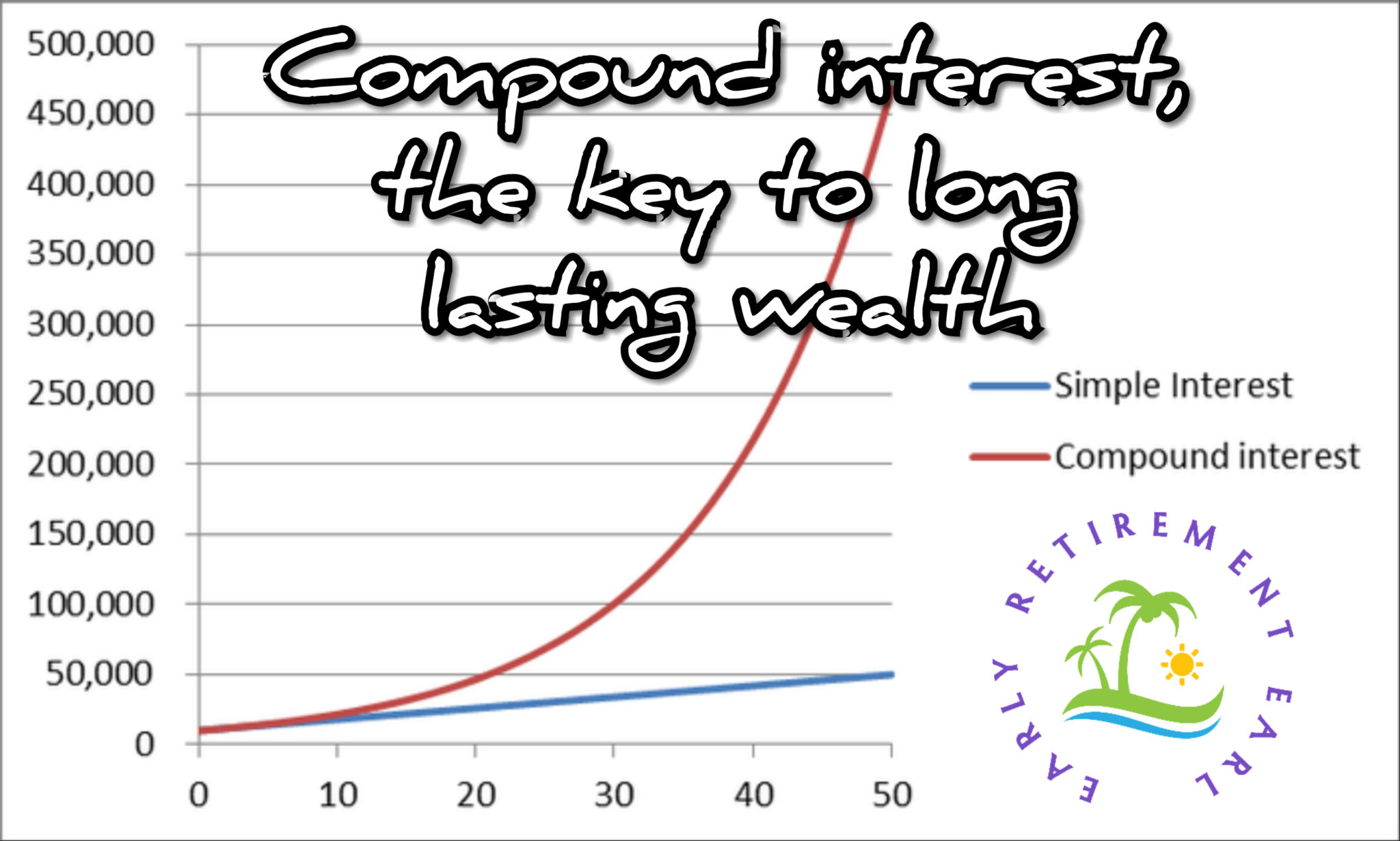

Step 7: The Power of Compound Interest

As your original post noted, Albert Einstein called compound interest the “most powerful force in the universe.” It’s the engine of your FIRE investment strategies.

How It Works

You earn interest on your principal, then interest on that interest, exponentially growing wealth. Example: $10,000 at 7% (compounded monthly) grows to $19,672 in 10 years, $38,697 in 20 years Bankrate Calculator.

FIRE Strategy

- Invest Early: Start with $500/month in VTI. At 7%, this grows to $104,000 in 10 years.

- Reinvest Dividends: Boost compounding by reinvesting ETF and stock dividends.

- Stay Consistent: Even $100/month compounds significantly over 20 years.

Link: How Compound Interest Will Make You Rich

Step 8: Sample FIRE Portfolio for 2025

Here’s a diversified gig economy FIRE portfolio for a $1M FIRE number:

- 60% Index Funds: $600,000 in VTI (growth).

- 20% Dividend ETFs: $200,000 in SCHD ($6,000/year income).

- 10% Blue-Chip Stocks: $100,000 in JNJ/PG ($2,500/year income).

- 5% REITs: $50,000 in VNQ ($1,750/year income).

- 5% Bonds: $50,000 in BND ($1,500/year income).

Total Income: $11,750/year, with growth to sustain 4% withdrawals ($40,000/year on $1M).Pro Tip: Rebalance quarterly to maintain allocations, using M1 Finance for automation.

Step 9: 12-Month FIRE Investment Action Plan

Here’s a 2025 roadmap:

- Months 1-3: Calculate your FIRE number. Open a Roth IRA and invest $1,000 in VTI.

- Months 4-6: Set up $500/month auto-investments in VTI and $100/month in SCHD.

- Months 7-9: Add $2,000 to VNQ. Research blue-chip stocks (JNJ, PG).

- Months 10-12: Invest $1,000 in BND. Review portfolio with a CPA for tax efficiency.

Step 10: Common Investment Pitfalls to Avoid

- Chasing Trends: Avoid crypto or meme stocks; stick to index funds and ETFs.

- Ignoring Fees: High-fee funds (1%+) erode returns. Choose VTI (0.03%) over mutual funds.

- Market Timing: Don’t wait for “perfect” entry points. Dollar-cost average instead.

- Underestimating Taxes: Use Roth IRAs or HSAs to minimize tax drag.

Link: 10 Insanely Easy Money Saving Techniques

Conclusion: Your FIRE Investment Journey Starts Now

Nobody achieves FIRE by accident. With FIRE investment strategies like index funds, dividend ETFs, blue-chip stocks, REITs, and bonds, you can build a $1M portfolio by 2030 to support a 4% withdrawal rate. In 2025, leverage low-fee platforms, tax-advantaged accounts, and compound interest to accelerate your financial independence investments

Take Action and Stay Focused

Earl

He didn't just save his way to freedom; he built a compounding engine. By combining "Bogleheads" index investing with a conservative options strategy, Earl turned a late start into a total victory. He’s not just talking theory—he’s living the math. Last year alone, Earl generated $78k in options premiums via the "Wheel" strategy and ~$400/month in passive dividends, proving that liquidity is the true key to quitting early.

Launched in 2019, EarlyRetirementEarl.com is a no-BS zone for dads and late-starters who want actionable, battle-tested steps to freedom. Featured on ThinkSaveRetire, ESI Money, Budgets are Sexy, and Camp Fire Finance, Earl’s mission is to share the financial literacy he was never taught in school. No fluff, no gurus—just the math.

Not financial advice. I’m not a CFP or licensed advisor. All numbers are historical; markets fluctuate. Past performance is not indicative of future results. Do your own research and consult a professional.