The Hidden Reason 80% of Financial Independence Retire Early Chasers Burn Out or Blow Up Their Savings

By Earl Owens | Read Time: 12 Minutes

The Lie That Kills Your Retirement

If you’ve been saving 40%, 50%, or even 70% of your income for more than three years, you know the drill. You’ve sacrificed, you’ve mastered VTSAX, and your net worth is climbing fast. You are a financial warrior.

But then, the dark days hit.

That moment in year five when you’re driving two hours out of your way to save $3 on gas, skipping your best friend’s destination wedding because the flight is “non-essential,” and staring at a $1.2M portfolio while wondering: What the hell am I doing all this for if I’m always miserable?

This feeling is not personal weakness. It’s the inevitable result of an aggressive, financially sound strategy crashing head-first into human psychology. It’s called Frugality Fatigue (FF), and it’s the number one killer of early retirement plans.

My Confession: How I Almost Blew $434,000 to Escape Frugality Fatigue

I know this burnout intimately. In 2020, I was 46, debt-free, with a solid $1.3M net worth. My savings rate was 45%, but my mental health was in the dumpster. My high-stress job was crushing me, and I hadn’t bought anything “nice” in years.

I felt entitled. I felt trapped.

The dam broke at the dealership. I went to the lot and nearly signed papers for an $80,000 Cadillac. The thought of finally treating myself to a luxury vehicle felt great, but I knew the guilt would follow. The mathematical guilt hit me: that $80,000, invested at 7% for 25 years, was $434,195 in lost freedom. I had nearly purchased a shiny dashboard in exchange for my future.

I walked away and instead bought another used Subaru, which I wrote a check for on the spot. I still drive that car today, and every time I turn the key, I am reminded of how close I came.

That decision was my wake-up call. I realized the car wasn’t about transportation; it was a symptom of my emotional exhaustion. The true fix wasn’t a massive splurge, but a Sustenance Line. I now reward myself with small, frequent treats, like my hobby of collecting watches, which is high happiness, low cost.

This post is your definitive guide to recognizing and fixing Frugality Fatigue before you burn out and make your own $434,000 mistake.

Part I: The Frugality Fatigue Curve (Why the Burnout is Inevitable)

Most financial blogs focus on External Lifestyle Creep (buying bigger houses, etc.). The real danger is Internal Lifestyle Creep—the slow, insidious neglect of your mental health, which eventually causes a catastrophic financial crash.

Defining Frugality Fatigue (FF)

Frugality Fatigue (FF) is the chronic mental and emotional exhaustion resulting from the sustained suppression of spending impulses and the constant, energy-draining need to optimize every minor financial decision. The research is clear: decision fatigue reduces willpower by up to 40% in just one day. Imagine seven years of it.

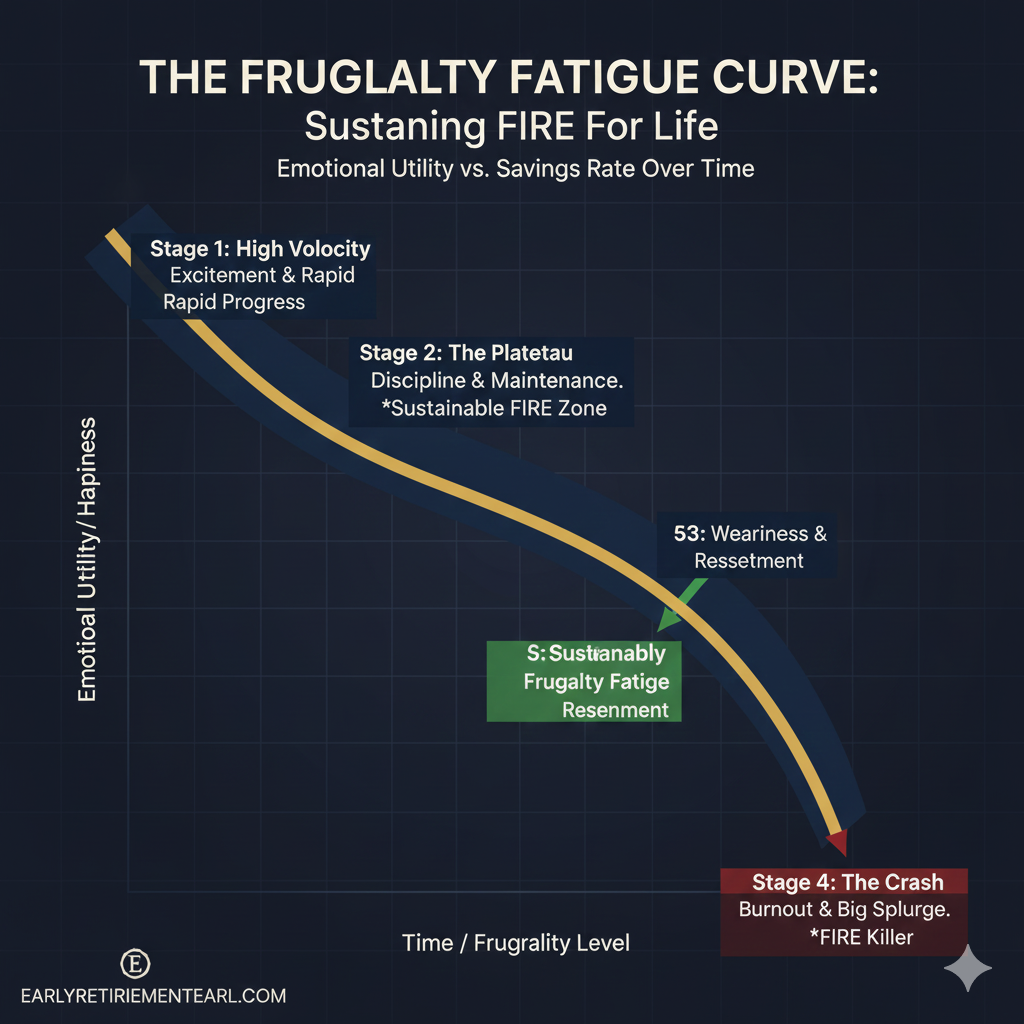

The 4 Stages of the Frugality Fatigue Curve

TL;DR: The goal is to avoid the Crisis Zone by maintaining emotional utility in The Plateau.

To combat FF, you must first visualize it. The Frugality Fatigue Curve maps your emotional utility against your savings rate over time.

1. High Velocity (The Honeymoon Phase)

- Vibe: Excited, obsessed, winning.

- State: Savings rate is spiking (50%+) because everything is new. The emotional utility of saving is very high.

2. The Plateau (The Sustainable Grind)

- Vibe: Disciplined, focused, but weary.

- State: The savings rate is stable, but the novelty is gone. Sacrifices feel routine and heavy. This is the critical maintenance zone.

3. Frugality Fatigue (The Crisis Zone)

- Vibe: Resentful, trapped, anxious.

- State: Cognitive Load Debt peaks. You obsess over minor expenses despite being wealthy. Emotional utility dips into the negative.

4. The Crash (The FIRE Killer)

- Vibe: Guilt, failure, relief.

- State: Impulsive quitting of the high-paying job or, as I almost did, a massive, irrational splurge (The FIRE Killer) to relieve pent-up pressure.

The goal is to operate sustainably in The Plateau forever.

Part II: Diagnosis – Are You in the Crisis Zone?

Before you can apply the fix, you need an honest assessment. You may be financially rich but mentally bankrupt.

The Non-Monetary Debt That Kills FIRE

TL;DR: The cost of Frugality Fatigue is the non-monetary debt you incur in time, mental energy, relationships, and health.

The cost of FF isn’t the money you save; it’s the non-monetary debt you incur. When this debt peaks, the system breaks.

| Non-Monetary Cost | Description | The Catastrophic Result |

|---|---|---|

| Time Debt | Spending hours to save dollars (e.g., driving 1.5 hours to save $15). | Wasted prime years; realizing time cannot be compounded. |

| Cognitive Load Debt | The mental energy spent on analysis paralysis over minor purchases. | Total mental shutdown, leading to impulsive high-cost spending. |

| Relationship Debt | Saying “No” to essential social spending, causing resentment and isolation. | Loneliness and strained relationships in early retirement. |

| Health Debt | Skimping on quality food, necessary medical/dental care, or gym memberships. | Higher long-term medical bills; poor quality of life after retirement. |

Frugality Fatigue Self-Assessment Checklist

TL;DR: A score of 7+ means you are in the Crisis Zone and need immediate intervention.

Answer honestly. If you check 4 or more, you are experiencing Frugality Fatigue. If you check 7 or more, you are in the Crisis Zone.

- Do you regularly decline social invitations solely due to cost, even though the expense is minor relative to your net worth?

- Do you spend more than two hours per week price-checking or couponing for items that cost less than $50 total?

- Do you feel anger or resentment when your partner or family buys something frivolous (even if it’s budgeted)?

- Do you have “analysis paralysis” when making a necessary purchase over $100?

- Is your relationship suffering because every conversation about money becomes a debate about sacrifice?

- Do you secretly resent your current high-paying job, even though it’s the engine of your freedom?

- Have you ever postponed a necessary health or dental checkup to avoid the co-pay?

- Do you constantly hoard free items (like condiments or samples) that clutter your life but offer negligible financial value?

- Do you often feel trapped, despite your growing net worth?

- Do you dream of making a massive, reckless purchase just to feel a moment of financial freedom?

Part III: The Sustenance Blueprint – 5 Strategies for Longevity

To shift your position on the Curve and prevent the crash, you must redefine frugality. These strategies involve re-allocating budget lines to buy back peace, time, and happiness.

Strategy 1: The Annual Budget Vacation (The Planned Splurge)

TL;DR: Schedule a single, high-impact splurge every year to relieve pressure and sustain your savings rate.

The psychological mistake is demanding 100% austerity. The solution is a Planned, Limited Breach.

- Define the Limit: Calculate 5% of your annual expenses. If you spend $60,000 annually, your limit is $3000 (The ABV Fund).

- Ring-Fence the Fund: This money must be tracked in a separate digital envelope. It is 100% guilt-free money.

- The Rule of One: Use the ABV Fund for one single, high-impact experience per year (e.g., a weekend cabin rental, a non-refundable course, or a new piece of gear for a core hobby).

The anticipation and the execution of the ABV act as a scheduled psychological decompression, proving that your hard work translates into tangible quality of life.

Strategy 2: The Time-Value-of-Money (TVM) Audit

TL;DR: Spend money when the cost of your time and stress outweighs the dollar amount saved.

Early in FIRE, your time is cheap. Later, your time is your most valuable asset. Use the TVM principle to justify spending that buys back time or reduces stress. Stress Tax Cost = Financial Value of Time Saved / Opportunity Cost of That Time

Actionable Example: The Grocery Run

- Frugal Way: 4 hours/week driving to 3 stores and prepping ingredients to save $20.

- TVM Audit Way: You spend $50 extra per month on a grocery delivery service. You buy back 6 hours of high-quality weekend time. You have purchased 6 hours of freedom for $8.33/hour. This is a brilliant investment.

Action: Identify three areas where you spend time and stress to save small amounts of money. Pay the money and buy your life back.

Strategy 3: The Sustenance Line (Non-Negotiable Self-Care)

TL;DR: Create 2-3 non-negotiable budget items that act as emotional insurance against a total mental collapse.

If you treat every budget line as equally cuttable, you’ll eventually cut the lines that keep you sane. A Sustenance Line is a small, protected budget item that prevents burnout.

- Identify the Antidote: What activity immediately reduces your stress and improves your mood? (e.g., a high-quality gym membership, weekly therapy, a cleaning service once a month, or my personal choice: premium coffee and financial research tools).

- Ring-Fence the Expense: Treat these 2-3 items as non-negotiable debt. They sit at the top of your budget before rent/mortgage and savings.

- The Rule of Protection: You do not cut the Sustenance Line until every other flexible expense has been eliminated. This line protects your emotional endurance, which is necessary to survive any crisis.

Strategy 4: The Reverse Budget (Automating Joy)

TL;DR: Pay your “Fun Fund” before you pay your high-percentage savings rate to eliminate the guilt of leisure.

The traditional FIRE budget mentally frames expenses as a cost against your goal. A Reverse Budget flips the script to reward you first.

- Automate Joy First: Set up a tiny auto-transfer (e.g., $100) into a separate “Fun/Hobby” checking account immediately after your paycheck hits.

- Automate Savings Second: Immediately execute the 50%+ transfer to your VTSAX brokerage.

- Spend What’s Left: Use your main account for all fixed expenses.

The Psychological Shift: By paying your Joy Fund first, you mentally treat it as a rewarded necessity. Since the major savings transfer has already happened, you have zero anxiety about the small amount remaining in the Fun Fund.

Strategy 5: The FIRE Re-Anchor (The Emotional Work)

TL;DR: Reconnect your current misery to a tangible, emotional outcome by visualizing your freedom.

The core reason FF sets in is that the goal ($2M in 10 years) becomes abstract.

- The Day-in-the-Life Journal: Write a hyper-detailed, sensory description of a perfect, financially independent Tuesday 10 years from now. Focus on feelings and sensations, not numbers.

- Example: “I wake up naturally at 7:30 AM to the smell of fresh coffee, not an alarm. My energy belongs to me. I feel the sun on my face. I have time.”

- The Re-Anchor Image: Find one single image that perfectly encapsulates that feeling. Print it out or save it prominently.

- The Daily Check-In: When FF hits—when you’re miserable or denying a small pleasure—read your journal entry. Reconnect the misery of the moment with the massive freedom that the sacrifice is buying.

Part IV: Sustaining Legacy & Avoiding the Horror Stories

The ultimate measure of FIRE success isn’t your net worth; it’s your ability to sustain the discipline long enough to get there.

Frugality vs. Happiness Matrix: The Smart Way to Spend

TL;DR: Cut everything in the Fatigue and FIRE Killer quadrants immediately.

Use this matrix to categorize your current spending and identify your FATIGUE ZONES.

| Quadrant | Cost Impact | Happiness/Utility Impact | Action | Result |

|---|---|---|---|---|

| The Sweet Spot | Low | High | KEEP & PROTECT | Highest ROI on happiness. |

| The Fatigue Zone | Low | Low | CUT IMMEDIATELY | Causes Frugality Fatigue. |

| The Smart Splurge | High | High | KEEP, BUT PLAN | The ABV Fund belongs here. |

| The FIRE Killer | High | Low | CUT IMMEDIATELY | Leads to massive regret. |

The Dark Side: When Frugality Kills Freedom

You need to know what a fatal crash looks like. These are anonymized stories from the FIRE community:

- John, Age 52 (Near FIRE): Hit $1.8M and quit his job, but the anxiety of frugality followed him. Out of sheer panic and boredom, he bought a $90,000 truck and RV combo—a desperate attempt to “feel rich.” He depleted his cash reserves and is now back at a low-stress job at age 58, working purely for income.

- Sarah, Age 38 (Early Quit): Saved 70% for five years, but the relationship debt was crushing her marriage. She quit her $200k job impulsively because she “couldn’t take the frugality anymore.” Now divorced and bartending to cover expenses, she threw away her Coast FIRE runway because her Sustenance Line was zero.

The Lesson: The money never bought them peace, because they never developed the mental infrastructure to handle the pressure. Check out more case study horror stories.

The Final Vow

Frugality is a tool, not a religion. It is a means to an end: Freedom. When the tool becomes the master, you lose the freedom you are fighting for.

Your goal is not just to retire, but to retire sane, happy, and well-adjusted. Protecting your emotional capital with a modest “Sustenance Line” is the best financial insurance you can buy.

Your challenge today is not to save more, but to spend strategically to sustain your savings habit.

Keep grinding, but also, keep living.

Your Golden Ticket

“Stop Guessing and Start Planning.”

Ready to be the Architect of your own future? Climb aboard the 48-lesson roadmap.

UNLEASH THE FINANCIAL FREEDOM COMPASSADMIT ONE | LATE STARTER EDITION

— Earl

He didn't just save his way to freedom; he built a compounding engine. By combining "Bogleheads" index investing with a conservative options strategy, Earl turned a late start into a total victory. He’s not just talking theory—he’s living the math. Last year alone, Earl generated $78k in options premiums via the "Wheel" strategy and ~$400/month in passive dividends, proving that liquidity is the true key to quitting early.

Launched in 2019, EarlyRetirementEarl.com is a no-BS zone for dads and late-starters who want actionable, battle-tested steps to freedom. Featured on ThinkSaveRetire, ESI Money, Budgets are Sexy, and Camp Fire Finance, Earl’s mission is to share the financial literacy he was never taught in school. No fluff, no gurus—just the math.

Not financial advice. I’m not a CFP or licensed advisor. All numbers are historical; markets fluctuate. Past performance is not indicative of future results. Do your own research and consult a professional.