Posted by Earl | October 2025

Imagine turning $50 a month into a pile of cash that lets you quit your job, travel the world, or just stop worrying about bills. That’s what investing can do, and you don’t need to be a Wall Street wizard to start. I was clueless in my 30s—thought “stocks” were for rich guys in suits. Then I put $100 into a simple investment and watched it grow to $5,000 in 10 years. Now, I’m on track to retire early, and you can be too. This 3,000-word guide is for total beginners who don’t know E-Trade from eBay. We’ll break down investing like it’s your first bike ride: wobbly but doable. With 2025’s tools (apps, low fees) and a little discipline, you’ll build wealth toward financial independence. Let’s dive in.

Why Investing Isn’t Just for Rich People

Investing is putting your money to work so it grows over time, like planting a seed that becomes a tree. In 2025, with credit card interest rates at 23.3% (per Bankrate) and savings accounts at 4.5% (Ally, Marcus), keeping cash in a regular bank account is like letting it rot. Investing can earn 7%+ annually, turning small savings into big bucks.

This guide is for you if:

- You’ve never invested and don’t know what “stocks” or “brokers” mean.

- You’re scared of losing money or think you need thousands to start.

- You want to save for a house, kids’ college, or early retirement (FIRE vibes).

We’ll cover 8 steps to start investing, with tables showing how $50/month grows, and tie it to your dream of financial freedom. No jargon, no suits—just real talk from a guy who started late and made it work.

The 8 Steps to Start Investing as a Beginner

- Understand What Investing Is

- Tackle High-Interest Debt First

- Build a Small Safety Net

- Open Your First Investment Account

- Pick Simple Investments (Stocks, Funds, ETFs)

- Master Compound Interest (See Tables)

- Automate Your Investing Habit

- Stay Calm and Plan for 2025’s Economy

Step 1: Understand What Investing Is

Investing is like renting out your money to companies or markets so they pay you back with interest or growth. Think of it as lending $100 to a business (via stocks or funds) that grows to $107 in a year.

Here’s the beginner’s breakdown:

- Stocks: You own a tiny piece of a company (e.g., Apple). If the company does well, your piece is worth more.

- Bonds: You lend money to a company or government, and they pay you interest (safer but lower returns).

- Funds/ETFs: Baskets of stocks or bonds, like a smoothie of investments, spreading risk (e.g., an S&P 500 fund owns 500 companies).

Why It Matters: In 2025, a regular savings account earns 0.5%, while investments average 7% (S&P 500 historical data). Over 20 years, $1,000 in a bank stays $1,100; invested, it’s $4,000.

Action: Write down why you want to invest (e.g., “retire at 50,” “buy a house”). This is your motivation. Share it in the comments to commit.

My Story: I thought investing was for rich folks until I learned $50 could buy a piece of the market. That shift started my path to financial independence.

Step 2: Tackle High-Interest Debt First

Before investing, clear debts with interest rates above 7% (e.g., 23.3% credit cards). Paying $100/month on a $5,000 card at 24% costs $1,200/year in interest—money you could invest. Low-interest debt (e.g., 3% mortgage) can wait.

Action: List your debts (use my Debt Payoff Guide):

- Focus on high-interest debt (credit cards, personal loans).

- Pay minimums on low-interest debt (student loans, car loans).

- If debt-free, skip to Step 3.

For Beginners: If you’re drowning in debt, invest $10/month to build the habit while paying off cards. Check Undebt.it to track both.

Pro Tip: Negotiate rates with creditors (see my debt guide) to free up cash for investing.

Step 3: Build a Small Safety Net

Investing is risky if a car repair forces you back into debt. A small emergency fund in a high-yield savings account (4.5% APY in 2025, per Marcus) keeps you safe. I started with $500 while paying off debt—it saved me when my car broke down.

Action: Open a high-yield savings account with Ally or Marcus:

- Save $25-$50/month until you hit $500-$1,000.

- Once secure, shift this money to investing.

For Low-Income Readers: Start with $10/month. Apps like Chime round up purchases to save painlessly.

Pro Tip: Keep this fund separate from your checking to avoid spending it.

Step 4: Open Your First Investment Account

An investment account is like a digital wallet for buying stocks or funds. You don’t need E-Trade (a platform for trading stocks) to start—modern apps make it easy. In 2025, 70% of new investors use mobile apps (per Fidelity).

Action: Choose one:

- Brokerage Account: Vanguard, Fidelity, or Charles Schwab for DIY investing. Free to open, no minimums.

- Robo-Advisor: Betterment or Wealthfront automates investing for 0.25% fees. Great for set-and-forget.

- Micro-Investing Apps: Acorns rounds up purchases to invest spare change (e.g., $3 coffee becomes $4, $1 invested).

How I Started: I opened an E-Trade account with $100, nervous as hell. Their app walked me through buying my first fund. Start with $50—no need to be fancy.Pro Tip: Compare fees on NerdWallet. Avoid platforms with high commissions (most are $0 in 2025).

Step 5: Pick Simple Investments (Stocks, Funds, ETFs)

Don’t chase TikTok stock tips—they’re traps. For beginners, stick to:

- Index Funds/ETFs: Own hundreds of companies (e.g., S&P 500 ETF like VOO). Low fees (0.03%), 7% average returns.

- Individual Stocks: Riskier but fun for learning. Buy one share of a company you know (e.g., $150 for Apple).

- Bonds: Safer, like lending money for 3-5% returns (e.g., BND ETF).

Action: Invest your first $50:

- Buy an S&P 500 ETF (e.g., VOO or SPY) through your brokerage.

- If using a robo-advisor, select “aggressive” for higher stock exposure.

- Avoid single stocks until you’ve got $1,000 saved.

Example: $100 in VOO in 2015 grew to $240 by 2025 (7% annualized). That’s $140 profit without lifting a finger.

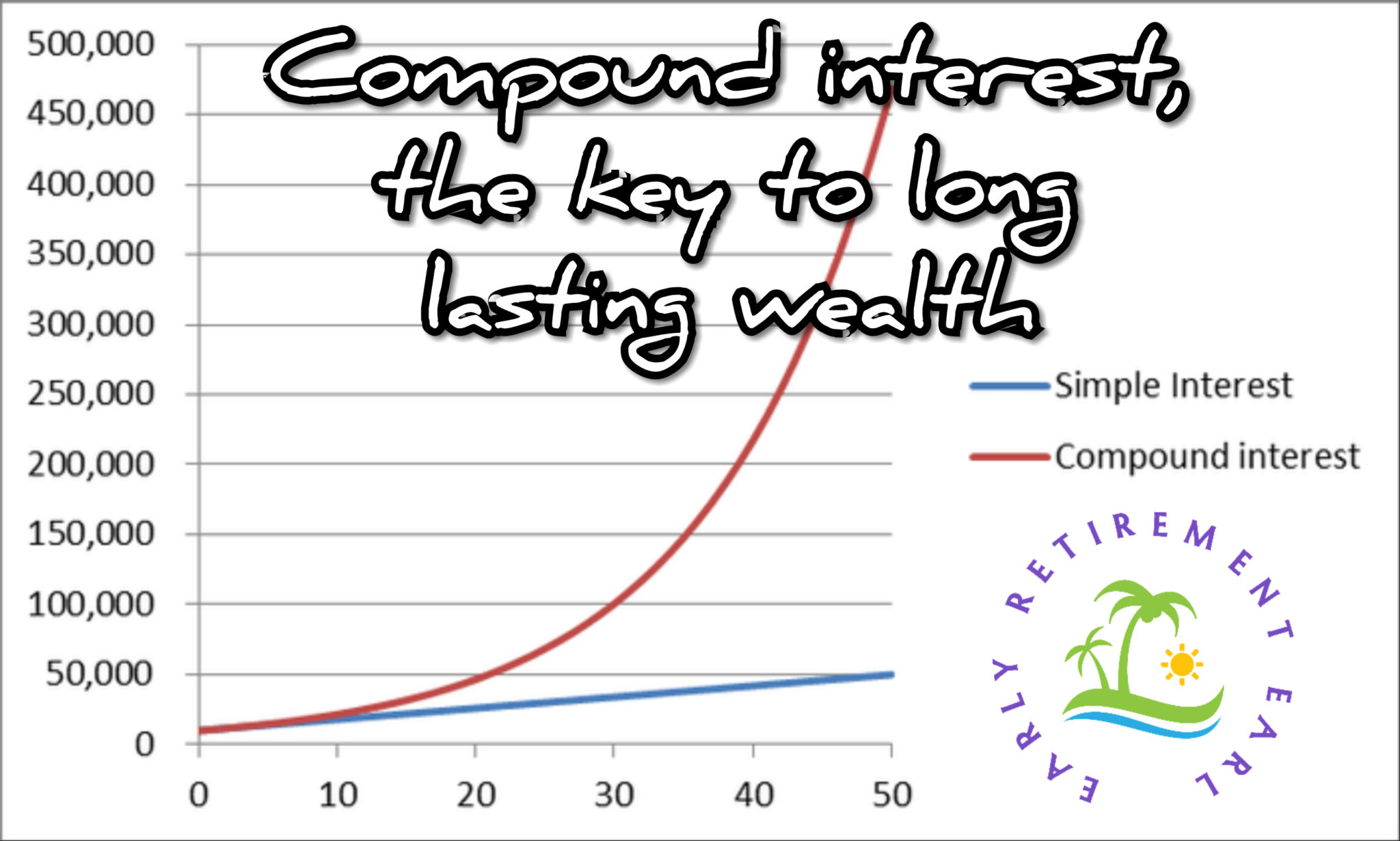

Step 6: Master Compound Interest (See Tables)

Compound interest is your money’s superpower—it grows on itself like a snowball. In 2025, with 7% average market returns, small investments become life-changing over time. Here’s how $50/month grows:

Table 1: $50/Month at 7% Annual Return (Compound Interest)

| Years | Total Invested | Value (7% Return) | Growth from Compounding |

|---|---|---|---|

| 5 | $3,000 | $3,563 | $563 |

| 10 | $6,000 | $8,627 | $2,627 |

| 20 | $12,000 | $26,033 | $14,033 |

| 30 | $18,000 | $56,617 | $38,617 |

Table 2: FIRE Goal Scenarios ($50/Month, 7% Return)

| Annual Expenses | FIRE Number (25x) | Years to Reach (w/ $50/mo) | Monthly Savings Needed (20 yrs) |

|---|---|---|---|

| $20,000 (Lean FIRE) | $500,000 | 50 | $800 |

| $40,000 (Standard FIRE) | $1,000,000 | 59 | $1,600 |

| $80,000 (Fat FIRE) | $2,000,000 | 67 | $3,200 |

Action: Use Investor.gov’s calculator. Input $50/month, 7%, and 20 years. Want your FIRE number ($1M) in 30 years? Save $500/month.

My Story: I started my E-Trade account late (age 43) and excelled with $1000/month at 45. At 7%, it’ll hit $500,000 by 65. Starting at 25 would’ve made me a millionaire by 55.

Pro Tip: Reinvest dividends to supercharge growth.

Step 7: Automate Your Investing Habit

Manual investing is like remembering to floss—easy to skip. Automate to make it effortless. In 2025, 60% of savers fail without automation (Fidelity data). I set up $100/month to Fidelity and watched it grow without thinking.

Action: Set up auto-transfers:

- $50/month to your brokerage or robo-advisor.

- Increase by $10/month annually (e.g., after raises).

- Track with Personal Capital.

For Beginners: Start with $25/month if $50 feels steep. Apps like Acorns automate spare change investing.

Pro Tip: Treat investments like a bill. Always pay yourself first.

Step 8: Stay Calm and Plan for 2025’s Economy

Markets swing—2022’s 20% S&P 500 drop scared me, but it recovered. In 2025, with 4-5% interest rates and 3% inflation, expect bumps but focus on the long game:

- Volatility: Keep 5-10% in bonds (e.g., BND) for stability.

- Taxes: Use Roth IRAs ($7,000 limit in 2025) for tax-free growth. HSAs ($4,300 limit) save for healthcare.

- Opportunities: High-yield savings (4.5%) for cash; ETFs for growth.

Action: Review investments yearly. If markets dip, keep investing—lower prices mean better deals. Use TurboTax for tax tips.

Pro Tip: Don’t check your account daily—it’s a rollercoaster. Focus on 5-year trends.

Beginner Scenarios

- Broke but Eager: Invest $10/month via Acorns while cutting $20/month.

- High Debt: Pay off >7% interest debt first, but save $25/month in a high-yield account.

- Late Starters (40+): Save 40%+ of income. Use IRA catch-up contributions ($1,000 extra if 50+).

- Side Hustlers: Invest gig income ($200/month from Uber Eats) in ETFs.

Mistakes to Avoid

- Hot Tips: Avoid crypto pumps or X-hyped stocks (e.g., 2021 meme stocks). Stick to funds.

- High Fees: Skip funds with >0.5% fees. VOO’s 0.03% is gold.

- Panic Selling: Markets drop—don’t sell. I held through 2022’s crash and recovered.

- Waiting for “Enough” Money: $50 starts the journey. Don’t delay.

The FIRE Connection

Investing is your ticket to Financial Independence, Retire Early (FIRE). The 4% rule says a $1M portfolio supports $40,000/year without depleting. Table 2 shows $50/month won’t get you there alone, but increasing to $500/month or starting at 25 can. My 7 Habits of the Rich shows how to save more to hit your FIRE number faster.

Your First Step to Wealth

Investing isn’t magic—it’s discipline and time. In 2025, with apps and low fees, anyone can start. My first $100 investment felt like a leap, but it grew to $5,000. Pick one action today: open an Ally account, set up $25/month to Acorns, or calculate your FIRE number. Share your step in the comments—I’m cheering you on.

Happy investing!—Earl

He didn't just save his way to freedom; he built a compounding engine. By combining "Bogleheads" index investing with a conservative options strategy, Earl turned a late start into a total victory. He’s not just talking theory—he’s living the math. Last year alone, Earl generated $78k in options premiums via the "Wheel" strategy and ~$400/month in passive dividends, proving that liquidity is the true key to quitting early.

Launched in 2019, EarlyRetirementEarl.com is a no-BS zone for dads and late-starters who want actionable, battle-tested steps to freedom. Featured on ThinkSaveRetire, ESI Money, Budgets are Sexy, and Camp Fire Finance, Earl’s mission is to share the financial literacy he was never taught in school. No fluff, no gurus—just the math.

Not financial advice. I’m not a CFP or licensed advisor. All numbers are historical; markets fluctuate. Past performance is not indicative of future results. Do your own research and consult a professional.